How to create a personal budget step by step for beginners, personal budgeting tips, beginner budget planning guide, money management strategies, and how to track expenses effectively are among the most searched financial planning topics today. Managing money properly is essential for achieving financial stability, reducing debt, and building long-term savings. However, many beginners struggle with budgeting because they don’t know where to start or how to maintain consistency.

Learning how to create a personal budget step by step for beginners allows individuals to control spending habits, prioritize financial goals, and reduce financial stress. Budgeting is not about restricting your lifestyle; instead, it helps you make smarter financial decisions and build a secure future.

This comprehensive guide explains budgeting fundamentals, step-by-step instructions, budgeting methods, common mistakes, practical examples, and expert strategies to help beginners build and maintain a successful personal budget.

What Is a Personal Budget?

A personal budget is a financial plan that tracks income, expenses, savings, and financial goals over a specific period. It helps individuals understand where their money goes and how to manage it effectively.

Key Components of a Personal Budget

- Income tracking

- Expense categorization

- Savings allocation

- Debt management

- Financial goal planning

Why Creating a Personal Budget Is Important

Budgeting provides financial clarity and helps prevent unnecessary spending.

Benefits of Personal Budgeting

- Improves financial control

- Helps reduce debt

- Encourages saving habits

- Prevents overspending

- Supports financial goal achievement

- Reduces money-related stress

Common Financial Problems Without Budgeting

Many people face financial difficulties due to lack of budgeting.

Typical Money Management Issues

- Living paycheck to paycheck

- Excessive credit card debt

- Lack of emergency savings

- Uncontrolled impulse spending

- Poor financial planning

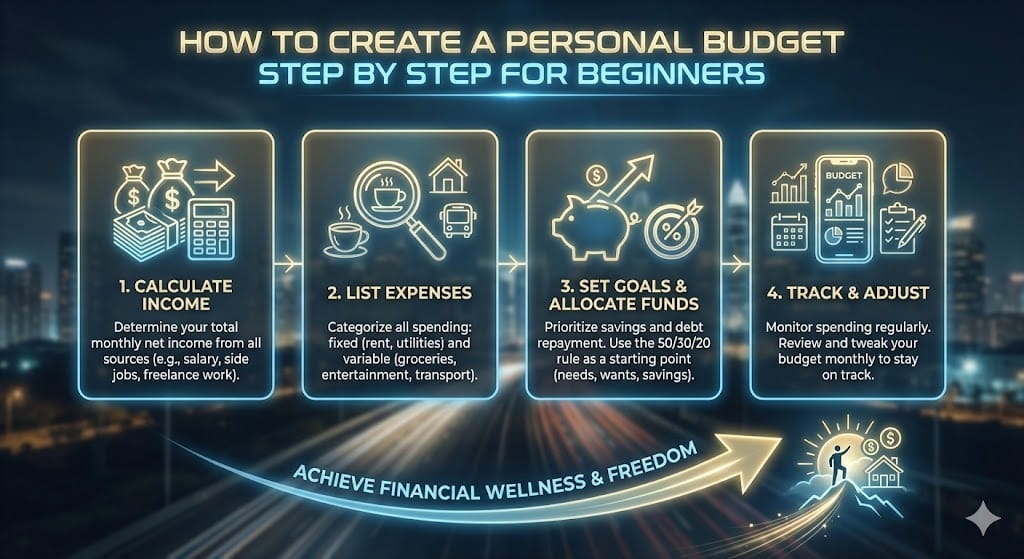

Step-by-Step Guide to Creating a Personal Budget for Beginners

Step 1: Calculate Your Total Monthly Income

The first step in budgeting is understanding how much money you earn each month.

Types of Income to Include

- Salary or wages

- Freelance income

- Business income

- Investment earnings

- Government benefits

- Side hustle earnings

Income Tracking Table Example

| Income Source | Monthly Amount |

|---|---|

| Salary | $2,500 |

| Freelance Work | $400 |

| Investment Income | $100 |

| Side Hustle | $200 |

| Total Income | $3,200 |

Tracking total income helps determine spending limits and savings potential.

Step 2: Track All Monthly Expenses

Understanding spending patterns is essential for building an accurate budget.

Types of Expenses

Fixed Expenses

- Rent or mortgage

- Insurance payments

- Loan payments

- Subscription services

Variable Expenses

- Groceries

- Utilities

- Transportation

- Entertainment

- Dining out

Expense Tracking Table Example

| Expense Category | Monthly Cost |

|---|---|

| Rent | $1,000 |

| Utilities | $200 |

| Groceries | $350 |

| Transportation | $150 |

| Entertainment | $120 |

| Subscriptions | $80 |

| Total Expenses | $1,900 |

Step 3: Compare Income and Expenses

Subtract total expenses from total income to understand financial balance.

Budget Balance Formula

Income – Expenses = Remaining Money

Example:

- Income: $3,200

- Expenses: $1,900

- Remaining: $1,300

Remaining money can be used for savings, investments, or debt repayment.

Step 4: Set Financial Goals

Financial goals provide direction and motivation for budgeting.

Types of Financial Goals

Short-Term Goals

- Building emergency fund

- Paying small debts

- Saving for vacation

Long-Term Goals

- Buying a house

- Retirement savings

- Education funding

Step 5: Choose a Budgeting Method

Different budgeting methods suit different financial lifestyles.

Popular Budgeting Methods

50/30/20 Budget Rule

| Category | Percentage |

|---|---|

| Needs | 50% |

| Wants | 30% |

| Savings and Debt | 20% |

Zero-Based Budgeting

Every dollar is assigned a purpose, ensuring income minus expenses equals zero.

Envelope Budgeting System

Cash is divided into envelopes for different spending categories.

Step 6: Build Emergency Savings

Emergency funds protect against unexpected financial crises.

Recommended Emergency Fund Size

| Financial Situation | Recommended Savings |

|---|---|

| Stable Job | 3 months of expenses |

| Freelancers | 6 months of expenses |

| High-Risk Income | 9 months of expenses |

Step 7: Reduce Unnecessary Expenses

Expense reduction increases savings potential.

Practical Cost-Cutting Tips

- Cancel unused subscriptions

- Reduce dining out frequency

- Compare service providers

- Buy generic products

- Limit impulse purchases

Step 8: Pay Off Debt Strategically

Debt management is essential for financial freedom.

Popular Debt Repayment Methods

Debt Snowball Method

- Pay smallest debt first

- Builds motivation

Debt Avalanche Method

- Pay highest interest debt first

- Saves more money long-term

Step 9: Track Spending Regularly

Consistent expense tracking maintains budgeting accuracy.

Expense Tracking Tools

- Budgeting apps

- Spreadsheet tracking

- Manual expense journals

- Bank expense categorization

Step 10: Adjust Budget Monthly

Financial situations change, so budgets must remain flexible.

When to Adjust Budget

- Income changes

- Expense increases

- New financial goals

- Economic changes

Beginner-Friendly Budget Example

Monthly Budget Sample

| Category | Allocation |

|---|---|

| Housing | $1,000 |

| Food | $350 |

| Transportation | $150 |

| Utilities | $200 |

| Entertainment | $150 |

| Savings | $800 |

| Debt Repayment | $300 |

Common Budgeting Mistakes Beginners Make

- Ignoring small expenses

- Setting unrealistic savings goals

- Forgetting irregular expenses

- Not tracking spending consistently

- Giving up budgeting too early

How Lifestyle Affects Budgeting Success

Lifestyle Factors

- Spending habits

- Social pressure

- Shopping behavior

- Financial discipline

- Income stability

How to Stay Consistent With Budgeting

Motivation Strategies

- Track financial progress visually

- Reward savings milestones

- Set realistic goals

- Automate savings transfers

- Review budget weekly

Best Budgeting Apps for Beginners

Popular Budgeting Tools

| App Name | Features |

|---|---|

| Mint | Expense tracking and budgeting |

| YNAB | Goal-based budgeting |

| PocketGuard | Spending limit alerts |

| EveryDollar | Simple zero-based budgeting |

How Budgeting Improves Mental and Financial Health

Budgeting reduces financial anxiety and improves financial confidence.

Psychological Benefits

- Reduces stress

- Improves decision-making

- Increases financial confidence

- Encourages responsible spending

How Income Level Affects Budgeting Strategies

Budgeting Based on Income Type

| Income Type | Budget Strategy |

|---|---|

| Fixed Salary | Stable monthly budget |

| Freelance Income | Flexible percentage budgeting |

| Seasonal Income | Emergency fund focus |

Advanced Budget Optimization Tips

Pro Budgeting Strategies

- Automate bill payments

- Use cash-back reward programs

- Negotiate service fees

- Track spending trends

- Increase income streams

How to Teach Budgeting to Family Members

Financial education improves household financial stability.

Family Budgeting Tips

- Set shared financial goals

- Create joint savings plans

- Teach children money management

- Track household expenses together

Long-Term Financial Planning Beyond Budgeting

Budgeting forms the foundation for advanced financial planning.

Long-Term Financial Strategies

- Investment planning

- Retirement savings

- Insurance planning

- Asset diversification

Estimated Financial Improvement After Budgeting

| Budget Consistency | Financial Improvement |

|---|---|

| 3 Months | Spending awareness increase |

| 6 Months | Debt reduction progress |

| 12 Months | Strong savings growth |

| 3+ Years | Long-term wealth building |

Signs Your Budget Is Working Successfully

- Consistent savings growth

- Reduced financial stress

- Improved spending control

- Achieving financial goals

- Reduced debt levels

When You Should Rebuild Your Budget

Rebuild or adjust your budget if:

- Income changes significantly

- Major life events occur

- Expenses increase unexpectedly

- Financial goals change

Future Trends in Personal Budgeting

Financial technology continues improving budgeting efficiency.

Emerging Budgeting Trends

- AI-powered budgeting tools

- Automated expense categorization

- Real-time financial tracking

- Personalized financial coaching apps

Conclusion

Understanding how to create a personal budget step by step for beginners is one of the most important financial skills anyone can learn. A well-structured personal budget helps individuals track income, manage expenses, reduce debt, and build long-term savings. Budgeting provides financial clarity, reduces stress, and supports financial independence.

By calculating income, tracking expenses, choosing the right budgeting method, and maintaining consistent financial discipline, beginners can build strong financial habits and achieve their financial goals successfully.

Frequently Asked Questions (FAQ)

How do beginners start budgeting?

Beginners should start by tracking income, listing expenses, and setting realistic financial goals before choosing a budgeting method.

What is the easiest budgeting method for beginners?

The 50/30/20 rule is considered the simplest budgeting method because it divides income into needs, wants, and savings.

How much money should I save monthly?

Financial experts recommend saving at least 20% of monthly income, but beginners can start with smaller amounts.

How often should I review my budget?

Reviewing your budget weekly or monthly helps maintain financial accuracy and spending control.

Can budgeting help reduce debt?

Yes. Budgeting helps allocate money toward debt repayment and prevents unnecessary spending.

Should I use budgeting apps or spreadsheets?

Both methods are effective. Apps provide automation and tracking convenience, while spreadsheets offer customization.