What does car insurance cover and what it does not, understanding car insurance policies, auto insurance coverage types, and exclusions are essential for every vehicle owner. With rising accident rates, vehicle theft, and expensive repair costs, having the right car insurance coverage is critical to protecting your finances and ensuring peace of mind.

Car insurance policies can be confusing due to multiple coverage types, legal requirements, and exclusions. Many drivers purchase insurance without fully understanding what is included, which can lead to unexpected out-of-pocket expenses after accidents or damages. Understanding what car insurance covers, what it excludes, and how to choose the right coverage is essential for both financial protection and compliance with legal obligations.

This comprehensive guide explains car insurance coverage, exclusions, optional add-ons, and strategies to maximize protection while minimizing unnecessary costs.

Why Understanding Car Insurance Coverage Is Important

Choosing the right car insurance policy protects drivers from financial loss and legal liability.

Benefits of Knowing Your Car Insurance Coverage

- Financial protection in accidents

- Protection against theft and vandalism

- Legal compliance with state requirements

- Reduced stress in vehicle damage situations

- Better decision-making when choosing policies

Key Car Insurance Terms You Must Know

| Term | Meaning |

|---|---|

| Premium | Monthly or annual payment to maintain coverage |

| Deductible | Amount paid out-of-pocket before insurance pays |

| Liability Coverage | Pays for damages to others if you are at fault |

| Collision Coverage | Pays for damages to your vehicle after a collision |

| Comprehensive Coverage | Covers non-collision damage like theft or natural disasters |

| Uninsured/Underinsured Motorist | Covers damages caused by drivers without insurance |

Step-by-Step Guide to Understanding Car Insurance Coverage

Step 1: Know the Types of Car Insurance Coverage

Car insurance includes various coverage types, each protecting against specific risks.

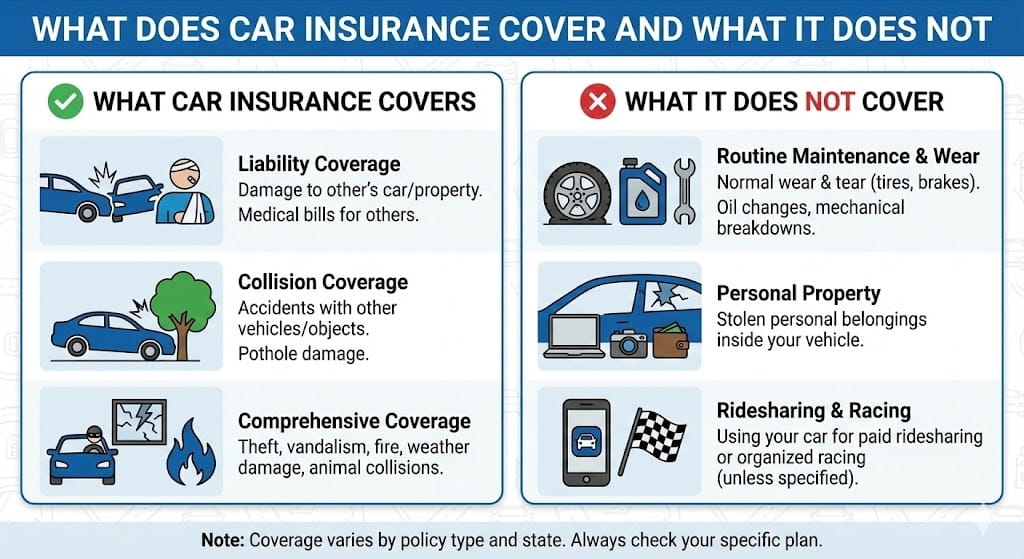

1. Liability Coverage

Liability coverage is often required by law.

- Bodily Injury Liability: Covers medical expenses, lost wages, and legal fees if you injure someone.

- Property Damage Liability: Covers repairs or replacement of another person’s property damaged in an accident.

Key Points:

- Mandatory in most states

- Protects you financially from lawsuits

- Does not cover your own car or injuries

2. Collision Coverage

Covers damage to your car resulting from a collision, regardless of who is at fault.

Key Points:

- Optional but highly recommended for financed or new vehicles

- Deductible applies

- Covers repairs or replacement of your vehicle

3. Comprehensive Coverage

Covers damage to your vehicle caused by non-collision events.

Examples of Covered Events:

- Theft

- Vandalism

- Natural disasters (floods, storms, earthquakes)

- Falling objects

- Fire damage

Key Points:

- Deductible applies

- Often required by lenders for financed vehicles

4. Uninsured/Underinsured Motorist Coverage

Covers damages when the other driver lacks adequate insurance.

Key Points:

- Protects your vehicle and medical costs

- Especially important in areas with high uninsured driver rates

5. Medical Payments / Personal Injury Protection (PIP)

Covers medical expenses for you and passengers after an accident.

Key Points:

- Some states require PIP

- Covers hospital bills, doctor visits, and sometimes lost wages

- Can extend to passengers in your vehicle

6. Optional Add-Ons

Optional coverage provides extra protection tailored to your needs.

Common Add-Ons:

- Roadside assistance

- Rental car reimbursement

- Gap insurance for financed vehicles

- Custom equipment coverage

- Accident forgiveness programs

Step 2: Understand What Car Insurance Does Not Cover

Knowing exclusions prevents unexpected out-of-pocket costs.

Common Car Insurance Exclusions

| Exclusion | Explanation |

|---|---|

| Intentional Damage | Any deliberate damage caused by the policyholder |

| Using Car for Commercial Purposes | Personal policies do not cover ride-sharing or delivery work |

| Wear and Tear | Mechanical breakdown, rust, or general maintenance |

| Racing or Illegal Activities | Damages incurred during illegal driving events |

| Driving Without a License | Insurance may deny claims if driver is unlicensed |

| Unreported Modifications | Unapproved aftermarket modifications may not be covered |

Step 3: Determine Your Coverage Needs

Coverage needs depend on car value, driving habits, and financial situation.

Coverage Decision Factors

- Age and condition of your vehicle

- State legal requirements

- Risk tolerance

- Daily commuting distance

- Financial ability to handle deductibles

Step 4: Compare Insurance Policies and Providers

Not all policies are created equal.

Factors to Compare

- Premium costs

- Coverage limits

- Deductible amounts

- Customer service and claim support

- Optional add-ons availability

Example Car Insurance Comparison Table

| Policy | Premium | Coverage Limit | Deductible | Add-Ons |

|---|---|---|---|---|

| Plan A | $120/mo | $50,000 liability | $500 | Roadside assistance |

| Plan B | $150/mo | $100,000 liability | $250 | Gap insurance + rental car |

| Plan C | $100/mo | $25,000 liability | $1,000 | None |

Step 5: Maximize Coverage While Minimizing Costs

Tips to Lower Premiums

- Increase deductibles if financially feasible

- Bundle auto insurance with home or renters insurance

- Maintain a clean driving record

- Take advantage of safety features discounts

- Pay annually instead of monthly

Step 6: Review Policy Annually

Insurance needs change over time.

Policy Review Checklist

- Vehicle value changes

- New drivers added to policy

- Updated driving patterns

- Premium rate changes

- State law changes

Step 7: File Claims Correctly

Proper claim filing ensures coverage is honored.

Claim Filing Steps

- Contact insurance company immediately

- Document accident with photos and notes

- Provide police reports if applicable

- Follow insurer’s instructions for repairs

- Keep all receipts and records

Common Mistakes to Avoid With Car Insurance

- Choosing the cheapest policy without evaluating coverage

- Ignoring exclusions

- Not reviewing policies annually

- Failing to update the insurer about car modifications or usage changes

- Overlooking optional coverage that could prevent high expenses

Car Insurance Coverage Checklist

| Coverage Type | Needed? | Notes |

|---|---|---|

| Liability | ✅ | Mandatory in most states |

| Collision | ✅ | Recommended for new/financed vehicles |

| Comprehensive | ✅ | Covers theft & non-collision damage |

| Uninsured Motorist | ✅ | High priority if area has uninsured drivers |

| Medical Payments / PIP | ✅ | Optional or required depending on state |

| Add-Ons | ⚪ | Tailor based on lifestyle & needs |

Understanding Liability Limits

Liability coverage protects against lawsuits and damages.

Typical Liability Coverage Structure

| Liability | Coverage Example |

|---|---|

| Bodily Injury per Person | $50,000 |

| Bodily Injury per Accident | $100,000 |

| Property Damage | $50,000 |

Choosing adequate liability limits is crucial for financial protection.

How Driving Habits Affect Coverage Needs

- Frequent commuting may require higher coverage

- Occasional drivers may opt for lower premiums with sufficient liability

- High-risk driving areas may require more comprehensive coverage

Future Trends in Car Insurance Coverage

- Usage-based insurance using telematics

- AI-assisted claims processing

- Increased coverage for electric vehicles

- Expanded telematics and monitoring discounts

Conclusion

Understanding what car insurance covers and what it does not is critical for financial protection, legal compliance, and peace of mind. Selecting the right policy involves evaluating coverage types, exclusions, deductibles, and additional benefits to ensure your vehicle and finances are protected. By comparing plans, reviewing coverage annually, and maximizing available discounts, drivers can enjoy comprehensive protection without overspending.

Car insurance is not just a legal requirement—it is a critical tool to protect your financial future and your safety on the road.

Frequently Asked Questions (FAQ)

What does standard car insurance usually cover?

Standard car insurance typically covers liability, collision, and comprehensive damages, depending on the policy.

Does car insurance cover personal belongings inside the car?

No. Personal items stolen from the car are generally not covered unless you have special add-ons or home insurance that extends coverage.

Are car insurance claims denied for accidents while racing?

Yes. Most insurance policies exclude damages resulting from illegal or high-risk activities like racing.

Can I add roadside assistance to my car insurance?

Yes. Roadside assistance is usually an optional add-on available with many policies.

How can I lower my car insurance premium without reducing coverage?

Increase deductibles, bundle policies, maintain a clean driving record, and take advantage of safety discounts.